Cryptocurrency: To See and Be Seen

Fierce debates are raging over how to regulate crypto markets. In a new publication, Jack Seddon and I reframe this as a battle over legibility.

In the mountains of Southeast Asia, where the borders of Thailand, Myanmar, Laos, and China collide, there are hundreds of villages populated by the Akha.1 The Akha are an ethnic group famous for their elaborate ceremonial dress. But they are also known for their resistance to state control. For over a hundred years, the geographical isolation of the Akha, in combination with their use of unwritten languages, allowed them to maintain high levels of political autonomy.2 They long avoided interaction with “lowlanders” and rejected efforts by the nation-states in which they ostensibly lived to subject them to legal classification.3 The Akha personified, in other words, the anarchist ideal of stateless society.

They still do. But government regulations on agricultural practices have lessened the capacity of Akha villages — which traditionally practice subsistence farming — to survive independently.4 Younger generations are also departing for larger towns to obtain formal education and pursue economic opportunities.5 Thus the Akha, which might be loosely compared to the Romani, Irish travelers, and the Amish, live in a state of tension. They are increasingly being pulled into the administrative orbit of national governments. And, in some cases, the Akha appear to see the benefits of that pull, taking steps to make themselves more understandable, and connected to, the state-dominated outside world. Yet they also engage in linguistic and cultural practices that guard against full integration.

In a new publication, Jack Seddon and I contend that indigenous ethnic groups are not the only communities experiencing this tension. There is another sector also living between worlds, one that has long been wrestling over whether to integrate into state structures: cryptocurrency.

To See and Be Seen

Like the Akha, cryptocurrency was originally dedicated to operating outside the confines of the state. Early innovations centered on the use of cryptographic methods (hence the name) to escape state surveillance. Bitcoin’s pseudonymous founder Satoshi Nakamoto summarized this goal in 2008, writing, “…we can win a major battle in the arms race [against the state] and gain a new territory for freedom for several years.”6 For many early developers and enthusiasts, cryptocurrency was not just a technological innovation but also an explicit political project with strong ties to anarchist concepts of stateless self-sovereignty.

In recent years, however, that community has reversed course, actively seeking state regulation and the validation it affords. The crypto industry now lobbies for clearer rules and permission to offer traditional financial products — most recently Exchange Traded Funds — to attract investors.7 This radical reversal is partly attributable to the changed make-up of the cryptocurrency “community,” which is now dominated by those more interested in financial opportunities than anarchist politics. But it also reflects a collective realization that regulation will help the market grow by making it easier for the public to participate.

Cryptocurrency, in sum, now wants to “be seen.” But it takes two to tango. The state is not obligated to recognize new markets. And, indeed, it may have incentives to simply look the other way. The state may, for example, hesitate to regulate crypto markets to avoid the responsibility to subsequently enforce those rules. Such oversight is costly. And, once the state establishes regulatory authority over a new market, it can then be blamed when things go wrong. States may also fear that regulation will afford legitimacy to risky products, encouraging elderly grandmothers with cataracts to put their life savings into cryptokitties.

Therefore, the integration of cryptocurrency markets into existing state structures is subject to two contrasting forces: the market’s desire to be seen and the state’s desire to see. Variations in these forces matter. They influence not just the growth of new markets but also how quickly they develop guardrails to protect investors and mitigate the risks of systemic financial crises. And, on a global scale, differences in states’ desire to “see” may create pockets of vulnerability where criminal actors can sidestep regulations. Inspired by sociology, we develop new terminology to explain these patterns: the supply and demand of market legibility.

Legibility and State Control

Imagine, for a moment, that you are an authoritarian dictator who has colonized a new territory full of gold mines — let’s call it Arrakis. Your first order of business, after deciding how many medals to place on your lapel, is to tax your new subjects. But there are problems. You discover that many residents of Arrakis do not have any form of legal identification. Making matters worse, they speak various dialects and have all sorts of local governing bodies with inconsistent rules. And despite the presence of gold deposits, they haven’t even built paved roads to mining sites. There are only inconsistent dirt paths winding throughout. Your aid says this is something to do with historic pathways to ‘religious’ sites. Whatever.

None of this will do. The lack of identification documents, in combination with the use of unknown local dialects, makes the population illegible to the state. The state cannot tax what it cannot measure. And those winding dirt roads make traffic unpredictable, undermining the state’s capacity to efficiently extract gold. The solution is simple: standardize. Outlaw dialects; mandate identification documents; create a national database of residents; clear the winding dirt roads and erect straight paved highways manned with cameras to monitor traffic. In sum, make Arrakis legible to the state to facilitate the imposition of your sovereign power.

This scenario exemplifies the oppressive nightmare envisioned by James C. Scott in his wonderfully-titled book, Seeing Like a State. For Scott, the state strives to make society legible through simplification and standardization, characteristics that render it more easily controlled. As he writes on city planning:

…state authorities endeavored to map complex, old cities in a way that would facilitate policing and control. Most of the major cities of France were thus the subject of careful military mapping (reconnaissances militaires), particularly after the Revolution. When urban revolts occurred, the authorities wanted to be able to move quickly to the precise locations that would enable them to contain or suppress the rebellions effectively.8

Those revolutionaries, in contrast, would prefer to remain illegible. Scott explores this concept further in The Art of Not Being Governed. This second book (with yet another fantastic title) focuses on how societies such as the Akha employ strategies of illegibility, such as living at high altitudes, practicing nomadic agriculture, and relying on oral histories, to pre-empt state control.9

For Scott, this is a one-directional relationship, in which the state imposes legibility on society. Later research has noted, however, that segments of society may sometimes desire legibility because it forces the state to address issues or recognize certain legal claims.10 Simultaneously, the state may hesitate to impose legibility for fear of what problems it may reveal. It is precisely these variations — and their combined impact on the regulation of financial markets — that we explore.

Making Markets Legible

Markets, like the Akha, can employ various strategies to make themselves more or less legible to the state. If, for example, they want to maintain their independence, they might develop terminology that the state does not understand: fork, gas, mining, beacon chain, bootnode, bytecode, HODL, MakerDAO. This is not just about using terms that befuddle geriatric politicians. It is language and concepts that cannot be easily reconciled with existing legal frameworks for market regulation. They are, in other words, illegible to the state.

If, in contrast, markets want to make themselves more understandable, they can engage in a process of translation. The introduction of intermediaries to crypto, such as brokers, exchanges, and fund managers, are examples. These are concepts that are easily recognizable to the state. The term “liquid staking” might draw blank stares from regulators, but if you rephrase this as the use of collateral, everyone is more likely to nod their heads and at least pretend they understand.

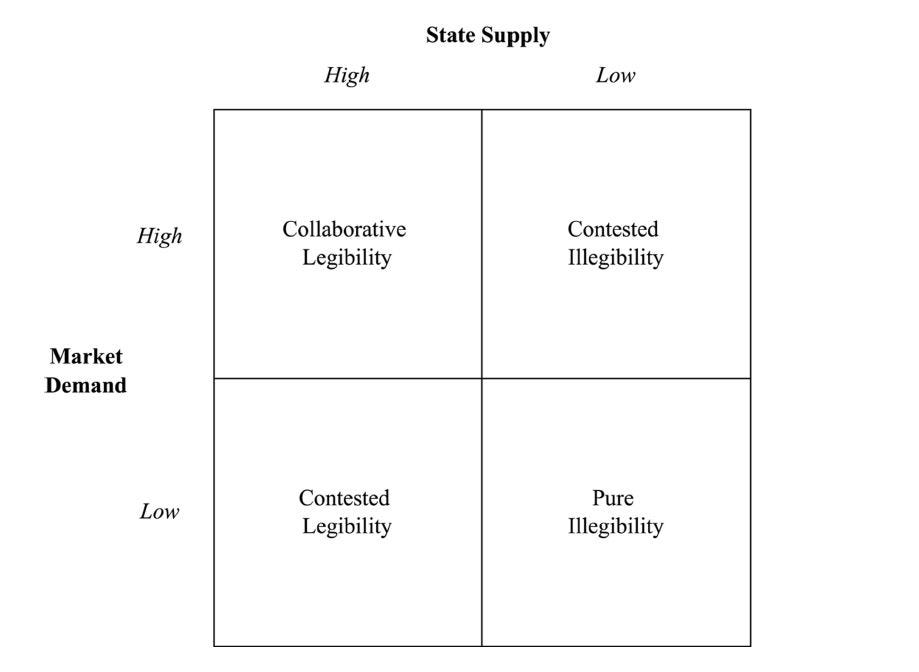

The strategies used by the market, and the response of the state, will naturally depend on whether each side desires to make the market legible. We indulge in one of the great guilty pleasures of political science to map this variation: the 2X2.

The four outcomes describe different conditions of market legibility. Most markets start in a condition of pure illegibility, in which neither industry actors nor the state is particularly interested in integrating the market into existing legal structures. This captures the early stages of cryptocurrency and most traditional markets. The New York Stock Exchange, for example, was once just a coffee house in Manhattan where brokers traded amongst themselves. For many years, neither these brokers nor the state had any interest in disrupting this system of private self-governance.

Markets might remain in this condition for long periods of time. Eventually, however, calls for legibility tend to emerge. Perhaps, for instance, some scandal occurs in the market, wiping out pension funds for hospital workers. This will put pressure on the state to intervene. They will, in other words, seek to make the market legible as a means of exerting greater control over its operations. If this outside interference is opposed by the industry, the market is in a condition of contested legibility (lower left-hand corner). In this scenario, industry players are contesting the state’s attempts to render their market more legible and thus subject to its authority.

Alternatively, calls for legibility may come from the market itself. There are many reasons the private sector may call for regulation. One example, alluded to above, is to make the market more accessible to public participation. Another possible driver is competition. If certain actors feel the informal rules of an unregulated market are unfair, they may appeal for state regulation as an equalizing strategy.11 But the state may not answer such calls. In this situation, the market is in a condition of contested illegibility (upper right-hand corner). The industry is, in other words, contesting the state’s refusal to integrate the market into existing legal structures.

Contestation, however, is unlikely to last forever. We anticipate that most markets will eventually make their way to the upper left-hand corner: collaborative legibility. In this situation, both the market and the state support legibility but simply disagree on the details. This disagreement may be intense. But there is an underlying commitment to operating the market within the administrative confines of the nation-state.

The Legibility of Cryptocurrency

In what stage is crypto? This depends on the jurisdiction. Markets in Europe, Japan, and the UK proceeded through different ‘stages’ of legibility, with consequences for how quickly they developed regulatory standards. Now, however, each is firmly in a condition of collaborative legibility. This is perhaps best exemplified by the EU, which has developed the world’s most comprehensive set of regulations on crypto-assets and related financial intermediaries.

The US, however, is a notable outlier. America is the world’s largest national market for cryptocurrency transactions, powered in large part by the entrance of big banks, asset managers, and other institutions from the ‘traditional’ finance world.12 And that growing industry has placed intense pressure on US regulators and policymakers to provide regulatory clarity. But the state has not answered these calls. To the contrary, it has largely exhibited an intense skepticism of, if not outright opposition to, the growth of Bitcoin and other digital assets.13

The US state’s hesitation to supply legibility was aptly demonstrated by the SEC’s recent approval of Bitcoin ETFs. The SEC long-resisted this step, refusing applications from various firms to offer ETFs on the grounds that they had taken insufficient steps to mitigate the risks of manipulation.14 One applicant, Grayscale, challenged this decision in court. To the SEC’s great annoyance, it won.15

The court’s decision forced the SEC to revisit applications and, on January 10th, it approved various Bitcoin ETFs for trading. But Chairman Gary Gensler’s statement on the approvals is written through gritted teeth:

While we approved the listing and trading of certain spot bitcoin ETP [Exchange Traded Products] shares today, we did not approve or endorse bitcoin…bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, money laundering, sanction evasion, and terrorist financing.

This is a great example of contested illegibility. The industry is demanding legibility from the state in the form of approving Bitcoin ETFs, going so far as to sue its own regulator in court. And even when the regulator is, in essence, forced to supply that legibility, it seeks to undermine the legitimacy of the very products it has just approved by telling investors to stay away.

If the history of cryptocurrency — and indigenous communities — is any guide, this period of contested illegibility won’t last. State and non-state worlds can often co-exist in a delicate equilibrium. But when one or both sides starts calling to merge those worlds, this creates a momentum that is very difficult to reverse. Thus, like the Akha, cryptocurrency is likely to continue its gradual drift from anarchy to control. Or, as we phrase it, out of the ether and into the state.

As described in James C. Scott’s The Art of Not Being Governed.

The Chinese government, for example, classifies the Akha as “Hani” ethnicity but this is often resisted. See also Deborah E. Tooker’s Modular Modern: Shifting Forms of Collective Identity among the Akha of Northern Thailand.

Here’s a nice documentary that captures the tensions of one Akha tribe between tradition and modernity.

ETFs are baskets of financial products that trade on the open market like a stock. As I write, there is hot anticipation that the SEC will soon approve the trading of crypto ETFs in the United States.

Seeing Like a State, 54-55.

Scott does, however, hesitate to classify the abandonment of texts and literacy as a purposeful strategy (Art of Not Being Governed, p. 220).

There’s a connection here to some the foundational strategic concepts explored by Albert O. Hirschman in Exit, Voice, and Loyalty.

For one summary, see Nizan Geslevich Packin’s Regulation By Enforcement And Crypto Assets.

For a summary of the case, see Grayscale, GBTC Litigation: Oral Arguments Unofficial Transcript.